Board-Ready Diagnosis

CFO · CEO · Board chair — walk into the board with a structural narrative, not a delta explanation.

The board doesn't want the variance walked. It wants to know whether leadership understands the structure underneath it.

The miss has happened. The board meeting is in two to four weeks. The CFO is the analytical lead in this moment; the CEO is the credibility-bearer. The board itself is the eventual audience — typically seven to twelve directors with mixed financial sophistication, mixed sector knowledge, and a duty to scrutinize. Their questions will be specific and adversarial: Why did this happen? How do we know it won't happen again? What changed in your assumptions? What are you doing differently? The standard move is a delta explanation — what changed versus plan, line by line. It rarely survives the second question.

Three things are at stake simultaneously: leadership credibility (whether the board treats the miss as an explainable episode or as a signal of deeper problems), strategic plan continuity (whether the board lets management adjust where needed without imposing an over-correction), and forward defensibility (whether the explanation given this quarter becomes a framework that holds up or one that breaks at the next quarter's results). Getting the explanation calibrated to the actual cause is what makes future board conversations easier rather than harder. Over-correcting damages the next four quarters; under-correcting damages the one after that.

Two patterns that produce over-correction the company pays for in future quarters.

The board will pressure management to do something visible about the miss. The two patterns below are how that pressure produces the wrong something — an over-correction that addresses the visible explanation rather than the structural cause.

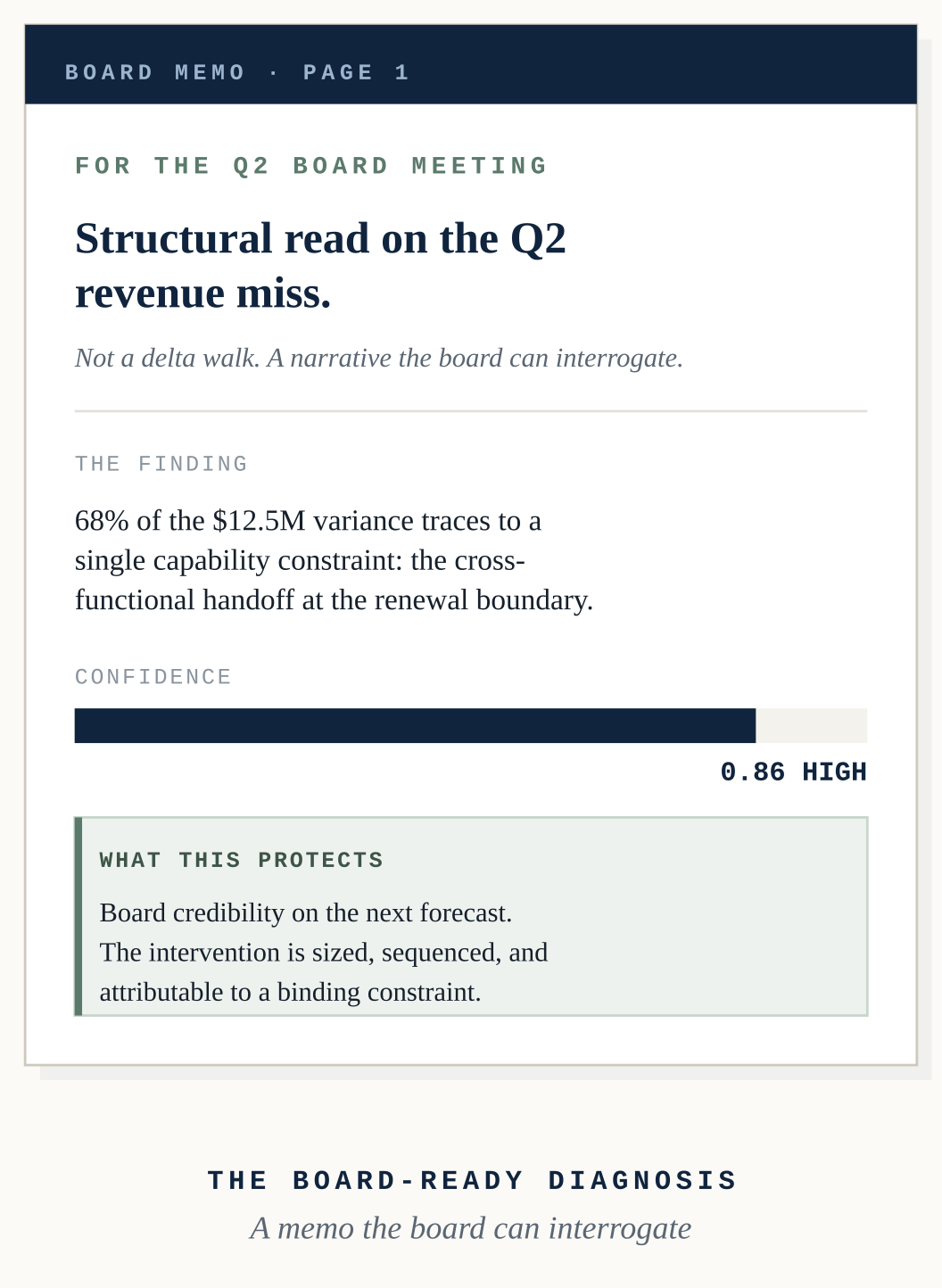

Both patterns share the same root: the explanation is calibrated to what is visible rather than to what is structural. The diagnostic work decomposes the variance into one-time / situational / structural categories with confidence classification on each — so the explanation matches the actual cause, and the corrective action targets the constraint that produced it.

A structural read on the variance, traceable to a binding constraint, defensible under board interrogation.

Zero Fog runs a focused diagnostic against the SEI substrate in the compressed two-to-four-week window before the board meeting. What actually happened, decomposed into one-time / situational / structural drivers with confidence classification on each. Why it happened — the causal chain from observed variance back to the capability constraint. Whether it will happen again — the forward signal the analysis gives about persistence. What the company should do about it — specific corrective actions tied to specific causal mechanisms, calibrated to the actual cause rather than over-corrected to whatever feels visible.

- Variance decomposition into one-time / situational / structural categories, with confidence-qualified findings at every node

- Causal chain from observed variance back to the binding capability constraint, with capability root named

- Persistence signal — whether the constraint will produce the same pattern again, with the timing surfaced

- Causality classification on every linkage; fog-qualified confidence on every finding — designed to hold up when a director asks a follow-up question

- Calibrated corrective action — sized, sequenced, and attributable to the binding constraint, with explicit avoidance of over-correction

- Defensible at the board meeting, the audit committee, and the next quarter's review when the framework gets re-tested

Engagement Shape

Best entry: Execution Diagnostic, scoped to the compressed pre-board timeline (typically 30 days for the variance analysis).

Common follow-on: A governed Quarterly Execution Cycle against the binding constraint, beginning the quarter after the board meeting.

Anchor artifact: A board memo — structural read on the variance, capability root named, confidence qualified, what-this-protects callout. The deliverable shown above.

Typical timeline: 2–4 weeks before the board meeting; renewable 90-day cycles thereafter, aligned to the board governance cadence.

Two ways forward.

Thirty minutes with the founder to discuss your board context directly. Senior practitioner on the call. No deck. The primary path for CFOs and CEOs with a board meeting in the next two to four weeks.

Request fit call →A self-guided session with our analytical substrate running on your company's profile, with the situational diagnosis matched to Pre-Board / Post-Miss. The path for prospects who want to experience the substrate before committing to a conversation.

Access the experience →Board-ready diagnoses frequently surface alongside one of these: